Recently we published a piece titled Why do many reasonable people doubt the science of investing? inspired by the lead article in the March 2015 issue of National Geographic. Over the next few days we will introduce some of the evidence that drives our conviction to follow a disciplined and evidence-based approach that is aligned with the science of investing. In this first installment we introduce the core principle of an evidence-based approach, risk and return, or more specifically, that expectations for investment returns are based only on expectations of risk. The remaining principles of the evidence based approach flow from this core principle.

Investment Returns are Related to Risk

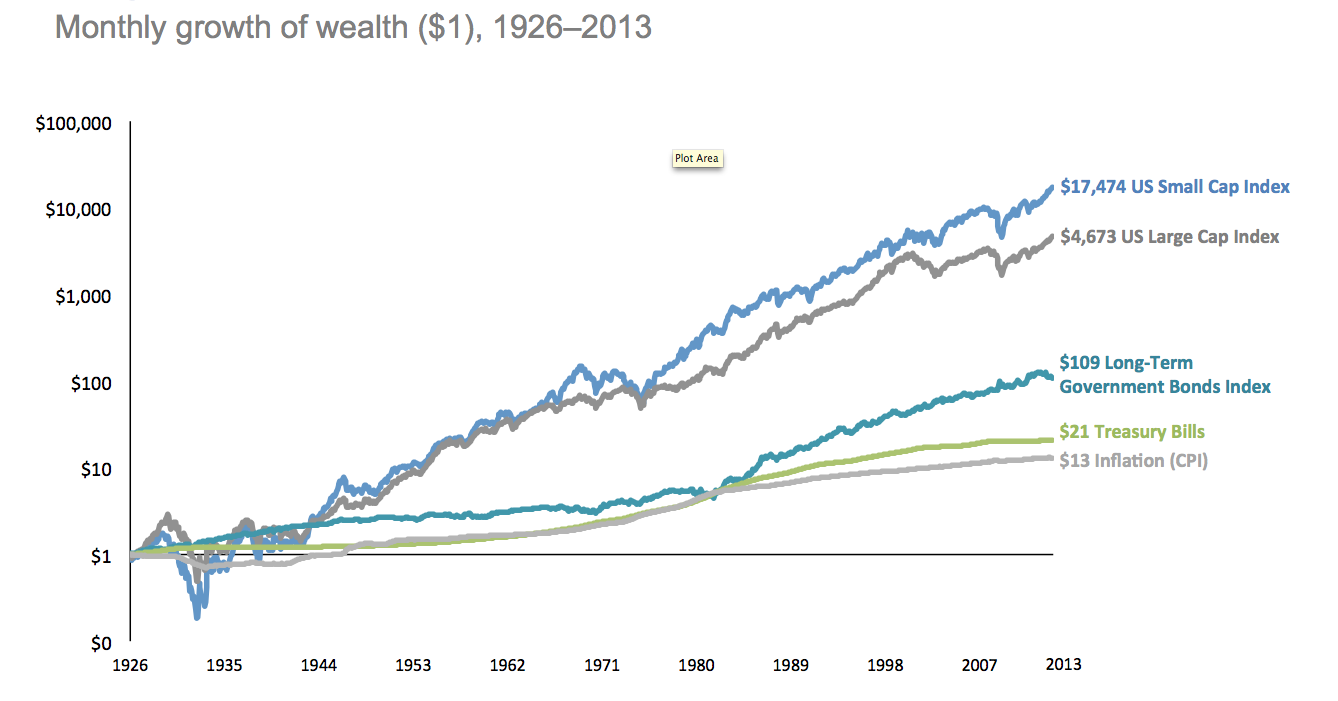

Investing should yield a return commensurate with the risk of that investment. Different types of investments or “asset classes” have yielded different rates of return over long periods of time. The following chart from Dimensional Fund Advisors (DFA) shows what would have happened if you had invested $1 in various US asset classes between 1926 and 2013. Stocks generally perform better than bonds over the long term. That shouldn’t be a surprise because stocks are riskier than bonds.

In the case of government bonds, where the safety of your investment is backed by the federal government, there is a strong likelihood that you’ll get your money back plus interest. Because government bonds have that safety attached to them, investors don’t require a very high rate of return on their investment. This is also why government bonds from Canada, for example, have a lower yield or interest rate than government bonds from Greece – the two countries have different levels of perceived creditworthiness so investors require different interest rates from their bonds. Stocks are riskier than bonds because they represent a share in the ownership of a company and owners are compensated only after all other stakeholders are paid including employees of the company, suppliers to the company, and those who’ve lent the company money. As the residual investor in the company, stock holders are paid last and therefore the investment carries a lot more risk. The chart above bares this out quite well. Over time, different types of investments with different risks require different rates of investment return to compensate investors.

The notion that risk and return are related goes back many years. Since the 1960s many academic studies have been conducted on the relationship between risk and return. Think of risk as a lack of certainty over how much money you’ll be left with at the end of your investment period, be that one year or thirty years. Risk is related to returns because investors decide what return they require to compensate them for taking on risk. In fact it is the collective impact of this risk/return assessment being performed by all the different investors in the market that ultimately sets a price for an investment. All the market participants, or investors, use all their knowledge and information to help them make decisions about expected risk and expected return and by doing so set a price. All these millions of transactions (chart below provided by the World Federation of Exchanges) conducted daily are done between willing buyers and sellers. They agree on a price to transact based on their collective knowledge and information about each investment.

In fact given this vast number of buyers and sellers of investments at any given time, the market price is a very efficient and powerful mechanism for reflecting all the collective information and expectations of all the different investors around the world. It is nearly impossible for any individual investor to be as good as the market at predicting the right price for an investment at any given time. Here is a fun activity that you can try with a group of people to try to replicate the power of markets.

In fact given this vast number of buyers and sellers of investments at any given time, the market price is a very efficient and powerful mechanism for reflecting all the collective information and expectations of all the different investors around the world. It is nearly impossible for any individual investor to be as good as the market at predicting the right price for an investment at any given time. Here is a fun activity that you can try with a group of people to try to replicate the power of markets.

How many jellybeans are in the jar? I suspect if you try this experiment you’ll come up with something similar – while the range of estimates is very wide, the average guess is very close to the actual number – the collective knowledge is stronger than that of the individual. Sure, perhaps somebody guessed closer, even bang on the actual number, but how easy is it to guess who’s a good guesser? That’s a good transition to the next principle of our Evidence Based Philosophy – that buying and holding the market (passive investing) outperforms trying to beat the market by stock picking or market timing (active investing) over the long run.

Please visit again for the next installment of Evidence Based Investing where we will discuss the next principle: Passive Investing Outperforms Active Investing.