Index investing means taking an automated or rules-based approach to constructing and managing a portfolio compared to active investing which relies on a portfolio manager’s judgement to manage the portfolio. There are many ways to implement an index approach. Most index funds follow a commercially published index like the S&P/TSX 60 in Canada or the S&P500 in the US. The individual securities represented in these indices are usually weighted by their market capitalization. Other approaches, while still very structured and systematic, try to weight the portfolio towards other “factors” that might yield returns higher than a simple market cap weighted index. For example research has shown that tilting an index towards smaller companies, cheaper companies or more profitable companies is likely to yield higher returns over time.

There has been a large increase in the number of these factor-based structured portfolio strategies in recent years. One factor that has commonly been used for decades is the value factor, essentially tilting a portfolio towards stocks with lower market valuations based on metrics like the price/earnings (P/E) ratio or the ratio of the book value to the market value of the stock. While the concept of value investing has been around for nearly 100 years and goes way back to the time of Benjamin Graham and David Dodd, original research published in 1992 by Eugene Fama & Kenneth French revealed the value factor to be systematically helpful and indeed index strategies developed since then have proven the research to be correct. A recent Morningstar article highlights that the Russell 3000 Value Index of US stocks outperformed the Russell 3000 Growth Index on average by 1.27% annually between 1978 and 2016. But look at the graph below:

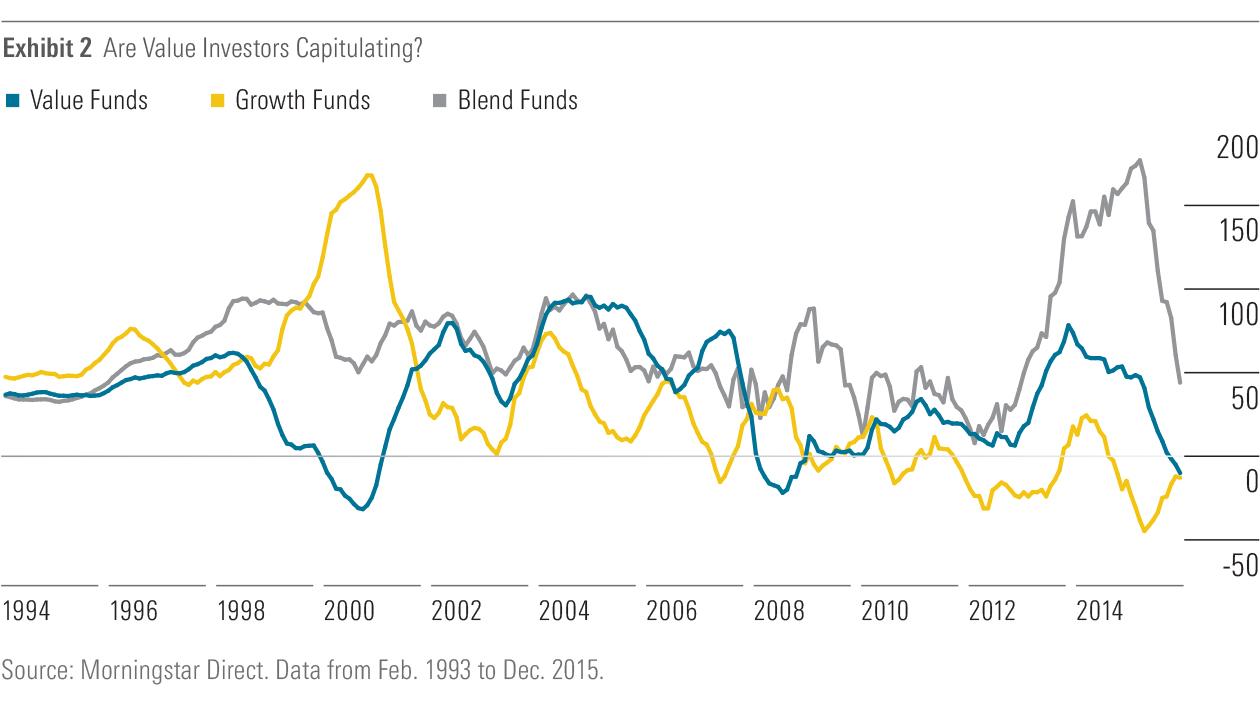

What happened to the value premium over the last 10 years? Have too many “smart beta” funds gotten wise to the idea and are now inflating the price of value stocks? Has something changed in the structure of the markets? While often investment strategies don’t quite tend to deliver the same performance shown in academic studies when actually put into practice, the value premium is one that has persisted for a long time. The reason it’s been able to persist and why other factors are able to persist is that they represent not only higher return but higher risk. Risk and return are linked closely and there is no free lunch with any of these factors. In order to benefit from factor returns over time, you are going to have to deal with periods of underperformance, sometimes painfully – that is the risk side! Now you don’t normally expect to see 10 years of underperformance but it’s not unheard of. It’s very difficult to try to time factor performance. Turnarounds can happen very quickly and returns to factors can accumulate over short periods of time – you have to stay the course to win. After 10 years it appears many aren’t willing to stay the course as the following chart from Morningstar shows – fund flows seem to indicate that value investors may be capitulating.

But isn’t this exactly the scenario that sets value up to outperform? Investors flee because they can’t bear the risk, leaving value stocks cheaper than ever. What’s happened since the beginning of the year? The Russell 3000 Value and Growth Indices have been running neck and neck with a slight edge to Value. It will be interesting to keep watching this one.

But isn’t this exactly the scenario that sets value up to outperform? Investors flee because they can’t bear the risk, leaving value stocks cheaper than ever. What’s happened since the beginning of the year? The Russell 3000 Value and Growth Indices have been running neck and neck with a slight edge to Value. It will be interesting to keep watching this one.